Form 6765 instructions guide businesses on claiming the federal R&D tax credit, detailing reporting, eligible expenses, and calculation methods to maximize tax savings. BooksMerge helps companies navigate this process with clarity and compliance. For professional assistance, call +1-866-513-4656.

Table of Contents

- Introduction to Form 6765

- What Is Form 6765 Used For?

- Who Qualifies for R&D Tax Credit?

- Understanding Qualified Research Expenses (QREs)

- Instructions for Form 6765 Step by Step

- How to Calculate ASC vs Regular Method

- Payroll Tax Offset for Startups

- What Changed in 2025 and 2026 Implications

- Required Documentation

- Conclusion

- FAQs

Introduction to Form 6765

Form 6765 plays a central role in claiming the IRS R&D tax credit. It is designed to reward businesses investing in innovation, whether improving products, processes, or software. While the form may seem intimidating, breaking it into sections reveals a clear process that businesses can follow. At BooksMerge, we see Form 6765 as more than paperwork; it’s a strategic tool that can reduce tax liability or generate payroll tax savings.

What Is Form 6765 Used For?

Form 6765 is used to calculate and claim the federal R&D tax credit under Internal Revenue Code Section 41. This credit rewards businesses that invest in qualified research, such as developing new products, improving processes, or enhancing software. Unlike a deduction, the R&D credit directly reduces the amount of tax owed.

Following the Form 6765 instructions is essential to ensure your claim is accurate and compliant. The instructions explain which expenses qualify, how to calculate the credit, and the differences between the regular credit method and the Alternative Simplified Credit (ASC). They also guide startups on applying the credit against payroll taxes if eligible.

Who Qualifies for R&D Tax Credit?

Businesses of all sizes can qualify, provided they conduct research activities that meet the IRS’s requirements. Eligibility criteria include:

- Developing or improving products, software, or processes

- Engaging in systematic experimentation to resolve technical uncertainty

- Relying on engineering, science, or computer science methods

Startups, manufacturers, and tech companies frequently qualify. Enhancing financial literacy improves understanding of such credits. Businesses can learn more about the importance of financial literacy in this Financial Literacy Statistics.

Understanding Qualified Research Expenses (QREs)

Qualified Research Expenses (QREs) are the foundation of Form 6765 calculations. According to IRS Form 6765 instructions, QREs include:

- Wages of employees performing or supporting research

- Supplies used during qualified research

- Contract research costs, typically at 65% of the expense

Non-qualifying costs include general overhead, marketing, and unrelated administrative expenses. Clear records of QREs reduce audit risk and simplify reporting.

Instructions for Form 6765 Step by Step

Form 6765 has four main sections:

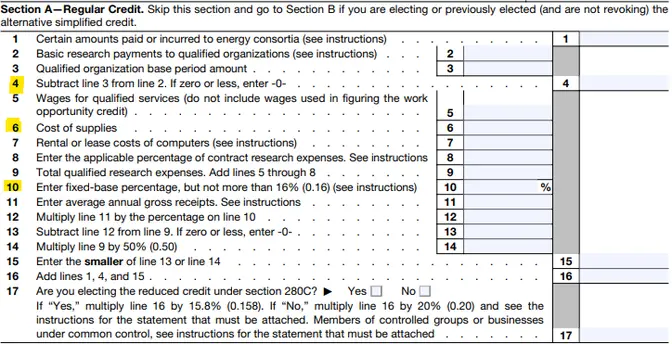

- Section A – Regular Credit Method: Uses historical QRE data to calculate the credit.

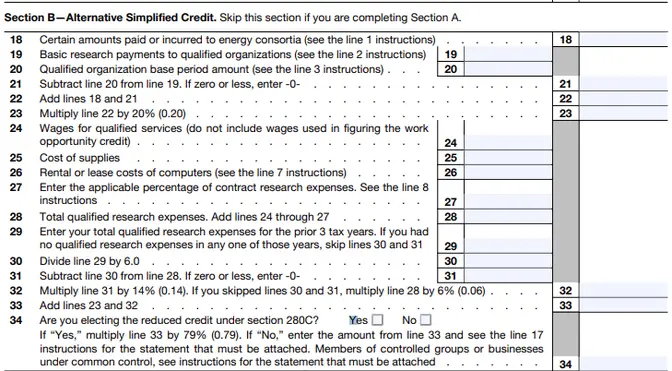

- Section B – Alternative Simplified Credit (ASC): Uses 14% of QREs above 50% of the prior three-year average.

- Section C – Additional Forms & Payroll Tax Election: For businesses electing payroll offset.

- Section D – Qualified Small Business Election: Enables startups to claim the credit against payroll taxes.

Businesses only complete sections relevant to their situation. Accuracy and complete documentation reduce the risk of IRS queries.

How to Calculate ASC vs Regular Method

The method you choose affects your credit amount:

- Regular Method: Compares current QREs to a historical base period; requires extensive prior records.

- ASC Method: Calculates 14% of QREs above 50% of the average of the previous three years; simpler for most businesses.

The choice should align with available documentation and long-term tax planning strategy.

Payroll Tax Offset for Startups

Eligible startups can apply the R&D credit against payroll taxes if they meet the IRS criteria:

- Gross receipts under $5 million

- Less than five years of operations

This allows startups to benefit even if they have little or no income tax liability, converting innovation into immediate cash savings.

Quick Tip: Understanding 1099 vs W-2 helps you decide between being a contractor with more flexibility or an employee with benefits and tax withholding.

What Changed in 2025 and 2026 Implications

The 2025 changes under Section 174 require businesses to capitalize and amortize R&D costs instead of expensing them immediately. This does not eliminate the R&D credit but increases the importance of accurate reporting. For 2026, businesses must ensure detailed documentation of research activities and costs to align with Form 6765 instructions.

Required Documentation

The IRS expects robust documentation to support R&D credit claims, including:

- Payroll reports and job descriptions

- Technical notes and project documentation

- Invoices for supplies and contractors

- Time tracking and allocation schedules

Maintaining contemporaneous records ensures compliance and strengthens your credit claim.

Conclusion

Form 6765 instructions provide a roadmap for claiming the IRS R&D tax credit. With careful planning, accurate documentation, and expert guidance, businesses can maximize tax savings and support innovation. BooksMerge helps companies navigate Form 6765 confidently and correctly. For assistance, call +1-866-513-4656.

FAQs

1.What is Form 6765 used for?

Form 6765 calculates and claims the federal R&D tax credit for qualifying research activities, reducing your federal tax liability.

2.Who qualifies for R&D tax credit?

Businesses conducting research to improve products, software, or processes may qualify, regardless of size or revenue.

3.What are QREs?

QREs include wages, supplies, and contract research costs directly related to qualified research activities.

4.How to calculate ASC vs regular method?

ASC uses a simplified formula based on recent QRE averages, while the regular method compares current QREs to historical data.

5.What documents are required?

Payroll reports, project documentation, invoices, and time allocation records support Form 6765 claims.

6.Can startups use payroll offset?

Yes, startups with gross receipts under $5 million and less than five years of operation can apply the credit against payroll taxes.

7.What changed in 2025?

R&D costs must now be capitalized under Section 174, increasing reporting requirements while maintaining the eligibility for Form 6765 claims.

Read Also: Form 6765 Instructions