Report Overview

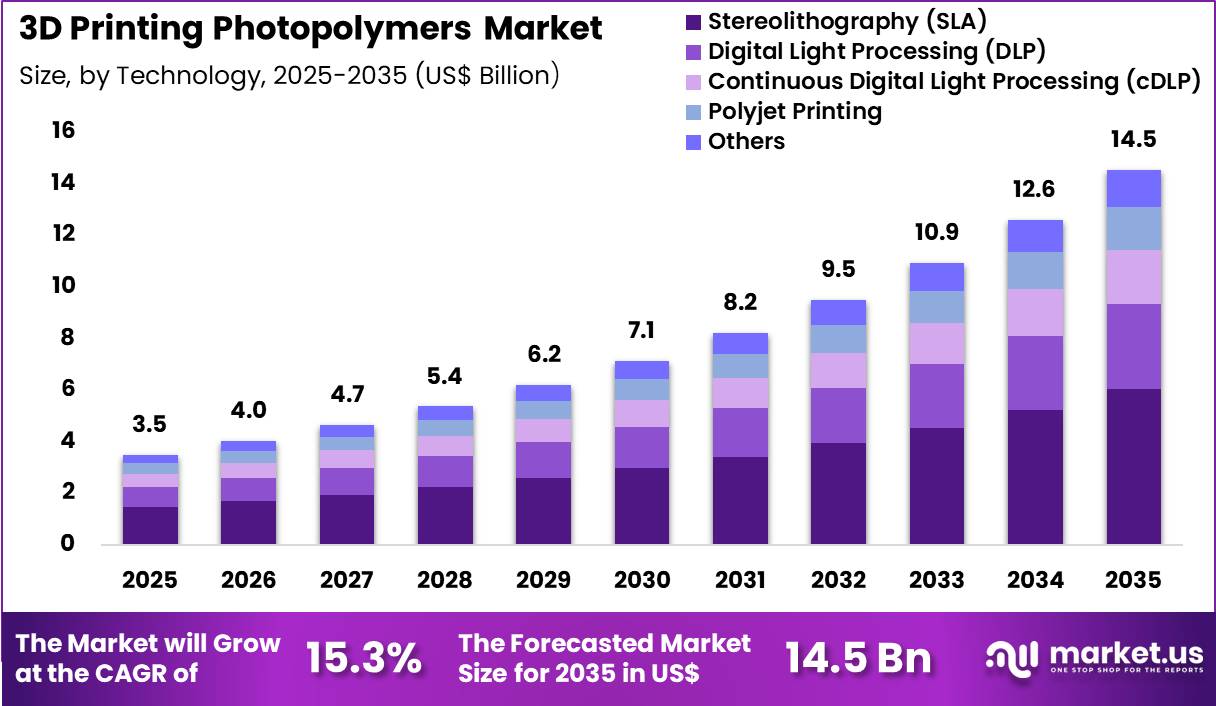

The Global 3D Printing Photopolymers Market size is expected to be worth around US$ 14.5 Billion by 2035 from US$ 3.5 Billion in 2025, growing at a CAGR of 15.3% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.4% share with a revenue of US$ 1.4 Billion.

Photopolymers for additive manufacturing represent specialized light-sensitive resin materials that undergo solidification when exposed to specific wavelengths of ultraviolet or visible light during the layer-by-layer fabrication process. These advanced polymer formulations enable the creation of highly detailed, complex geometric structures with superior surface quality and dimensional accuracy compared to many traditional manufacturing techniques.

The technology facilitates rapid prototyping, functional part production, and custom manufacturing across diverse industrial applications. Photopolymer materials offer exceptional resolution, smooth surface finishes, and the ability to produce intricate features that would be challenging or impossible with conventional methods.

As a result, these materials deliver significant value for product development, manufacturing tooling, medical device production, dental applications, jewelry fabrication, and precision engineering components.

Industry professionals increasingly adopt photopolymer-based additive manufacturing systems because they provide faster iteration cycles, reduced material waste, and greater design freedom, resulting in more efficient product development processes. These systems help connect conceptual design stages with final production by generating physical parts that accurately represent digital models.

Standard photopolymer techniques encompass stereolithography (SLA), digital light processing (DLP), material jetting, and continuous liquid interface production (CLIP). These methods enable the formation of precise layered structures while maintaining consistent mechanical properties and aesthetic qualities.

As market demand increases for customized products and agile manufacturing solutions, photopolymer-based additive manufacturing continues to expand across aerospace, automotive, healthcare, consumer goods, and industrial equipment sectors, driving innovation in on-demand production and next-generation manufacturing capabilities worldwide.

Click here for more information: https://market.us/report/3d-printing-photopolymers-market/

Key Takeaways

- The photopolymer additive manufacturing market stood at USD 458.9 million in 2025 and is forecast to achieve USD 1,247.3 million by 2035, advancing at a CAGR of 10.5%.

- Standard liquid resins commanded the material type segment, representing a 61.3% market share in 2025.

- Prototyping and product development led the application segment, comprising 34.6% of the market.

- Manufacturing and production firms constituted the largest end-user segment, generating 49.6% of total market revenue.

- North America established itself as the premier regional market, claiming 39.6% of the worldwide market share.

Key Market Segments

By Technology

- Stereolithography (SLA)

- Digital Light Processing (DLP)

- Continuous Digital Light Processing (cDLP)

- PolyJet Printing

- Others

By Application

- Dental

- Medical and Healthcare

- Audiology

- Jewellery

- Automotive

- Prototyping

- Industrial and Engineering

- Electronics

- Others

By Performance Type

- Low Performance

- Mid Performance

- High Performance

Top Key Players

- Stratasys Ltd.

- 3D Systems Corporation

- Formlabs Inc.

- Henkel AG & Co. KGaA

- BASF SE

- Arkema S.A.

- Evonik Industries AG

- Carbon, Inc.

- Keystone Industries

- Shenzhen Esun Industrial Co., Ltd.

- Liqcreate

- Photocentric Ltd.

Emerging Trends in the Photopolymer Additive Manufacturing Market

- Manufacturers are increasingly developing application-specific photopolymer formulations to address specialized industrial requirements. Advanced material development initiatives aim to produce hundreds of customized resin variants, enhancing performance characteristics and expanding application possibilities across multiple sectors.

- Regulatory bodies are establishing standardized testing protocols for photopolymer materials. Recent guidance frameworks support comprehensive material characterization methodologies, including mechanical property verification and biocompatibility assessment, to generate reliable performance data for critical applications.

- High-performance engineering photopolymers with enhanced mechanical properties are emerging as significant innovations. Recent developments have introduced temperature-resistant and impact-resistant formulations with functional durability, helping engineers create production-ready components for demanding operational environments.

- Integration of automated post-processing systems with photopolymer printing workflows is expanding rapidly. New streamlined production platforms are being designed to handle thousands of parts efficiently, improving throughput, consistency, and automated quality verification.

- Manufacturing applications are shifting toward production-grade photopolymers. Industry repositories have established extensive material databases with comprehensive performance specifications, enabling engineers to select appropriate formulations with higher confidence for end-use applications.

Major Use Cases of Photopolymer Additive Manufacturing

- Rapid prototyping represents a primary application. Photopolymer systems enable designers to produce functional prototypes with accurate geometries and surface finishes, allowing teams to evaluate form, fit, and function before committing to expensive tooling investments.

- Customized manufacturing programs utilize photopolymer technologies to produce patient-specific medical devices and dental prosthetics. These capabilities support personalized treatment approaches and address the increasing demand for tailored solutions in healthcare applications.

- Tooling and fixture production extensively relies on photopolymer additive manufacturing. Engineers use these materials to fabricate jigs, fixtures, and assembly aids under conditions that reduce lead times and costs compared to traditional machining methods.

- Functional testing is increasingly performed using photopolymer components. Engineering-grade formulations can withstand operational stresses for extended periods and provide performance data that traditional prototyping materials cannot deliver.

- Small-batch production is benefiting from advanced photopolymer systems. Industry adoption metrics show substantial growth in production applications, with thousands of manufacturers utilizing these technologies for on-demand component fabrication, demonstrating strong commercial viability.

Conclusion: The photopolymer additive manufacturing market is positioned for substantial expansion, fueled by rising demand for advanced production technologies in prototyping, custom manufacturing, medical applications, and precision component fabrication. The technology's capability to deliver high-resolution parts with complex geometries makes it an essential tool for modern product development and specialized manufacturing.

With the market anticipated to grow from USD 458.9 million in 2025 to USD 1,247.3 million by 2035 at a CAGR of 10.5%, opportunities are broadening across manufacturing, healthcare, aerospace, and consumer product industries. Ongoing advancements in material formulations, automated processing systems, and production-grade applications are expected to further accelerate market penetration globally.